The Trump Administration’s trade policy is the bright fire that sparked a thousand topics: consumer goods, reshoring, rare earth minerals, labor shortages and the future of the economy, to name just a few. But for many Northeast Wisconsin manufacturers, the unpredictable tariff news has created a storyline defined by uncertainty.

As you read this month’s cover story, you’ll see that some of our state’s sharpest business minds share a lot of that uncertainty. From on-the-ground accounts of how manufacturers are responding to tariffs to practical advice on maintaining a solid trade strategy for your business in the face of change, these essays are defined not as much by uncertainty as authenticity.

The wisdom and candor they impart can lead to conversation. And in times of uncertainty, conversations matter. I thank all six of them for sharing their perspectives on this challenging topic.

Adapting to ‘America First’ in a shifting trade landscape

by Ngosong Fonkem, Partner, Amundsen Davis Law

The trade tensions between the U.S. and China that began as a dispute under the first Trump Administration have evolved into a deeper geopolitical rivalry that encompasses technology, national security and global leadership.

To stay competitive, U.S. businesses must understand the implications of this new reality and develop strategies to adapt and thrive in this shifting global trade environment.

President Trump entered his first term in the White House as a political outsider with no prior government experience and a bold promise to reshape the U.S. trade relationship with China. However, without a cohesive and experienced team, Trump’s “America First” trade policy focus on China was marked by abrupt decisions and uncertainty for American industries.

The administration came back into office for a second term with a much more coherent and methodical trade plan. That plan? To prioritize strict enforcement of U.S. trade laws against China. This was made clear Nov. 26, 2024, when then-President-Elect Trump promised to sign an executive order that would impose additional 10% tariffs on all imports from China his first day in office. These threats were realized Feb. 1, when Trump signed an order imposing 10% tariffs in addition to the existing 25% tariffs on imports from China. The additional tariffs were thereafter increased to 20% March 5.

The tariffs were issued amid two executive orders (EOs) that aimed to define the strategies underpinning Trump’s trade policies. The first of those instructed the U.S. Trade Representative to, within 180 days:

- review on a country-by-country basis and identify those countries that imposed higher import tariffs than the U.S. in their bilateral trade dealings;

- and recommend tariffs on a country‑specific basis

The second EO outlined the administration’s goals and parameters for crafting its “America First” trade policy. It instructed key agencies to investigate specific concerns, including the persistent trade deficit; the U.S. export control system; and the feasibility of establishing an External Revenue Service to collect tariffs, duties and other foreign trade-related revenues, and to present their findings. These findings, along with other trade actions — such as restrictions on the sale of certain critical technologies to China and several trade investigations against China — would form the basis for the Trump Administration’s choice of trade actions and remedies for redressing perceived economic grievances.

The first of such trade actions occurred April 2 — the so-called Liberation Day — and signaled a new phase in U.S. trade policy with the implementation of significant reciprocal tariffs on all imports from various countries to the U.S. These tariffs ranged from a baseline rate of 10% on imports of most goods to higher rates based on trade imbalances. In the case of China, those tariffs were assessed at 34% and led to retaliation with China’s own reciprocal tariffs. Moreover, in response to ongoing export restrictions on certain critical technologies to China, the Chinese government imposed export control restrictions on select critical minerals destined for the U.S. This tit-for-tat retaliation escalated, increasing costs for U.S. businesses and consumers, disrupting global supply chains and injecting uncertainty into the economy. The ensuing chaos led to an effective embargo between the U.S. and China. As a result of the disruption to the U.S. economy, both sides agreed to reduce reciprocal duties to 10% for a 90-day period and temporarily eased the restrictions on rare earth minerals and certain semiconductor chips pending further negotiations. These facts remain unchanged as of press time.

In the near term, companies must retool their import and export strategies by exploring inbound and outbound tariff mitigation based on business and sales transaction flows.

While these measures may not eliminate the impact of tariffs altogether, they can significantly soften the blow and preserve their competitiveness. In the long run, U.S. companies need to address the mounting challenges associated with their China-based operations and customers. That similarly requires balancing the cost advantages of operating in China with the rising risks to make proactive, informed decisions that align with their long-term global strategies.

The trade war between the U.S. and China has reshaped the way U.S. companies must operate on the global stage. While the challenges are substantial, so too are the opportunities for those who act decisively. The path forward requires adaptability, innovation and a pragmatic implementation of long-term strategy.

Econ 101: On trade and tariffs

by Marc von der Ruhr, Professor of Economics, St. Norbert College

As an economist trained in international trade, it is interesting to observe the difference between the economics of trade and the public perception of trade. The Venn diagram of these two perspectives shows very little overlap. And I think I know why: The costs of international trade are concentrated (it makes the news when RCA moves its production of TVs from Indiana to Mexico), but its benefits are diffuse (rarely do people, as they check out at their local store, acknowledge that they would pay more for a TV if it were manufactured in the U.S.). A further issue is that the outcomes of trade policy are a function of many voices at the bargaining table, and policy outcomes may not represent economic ideas.

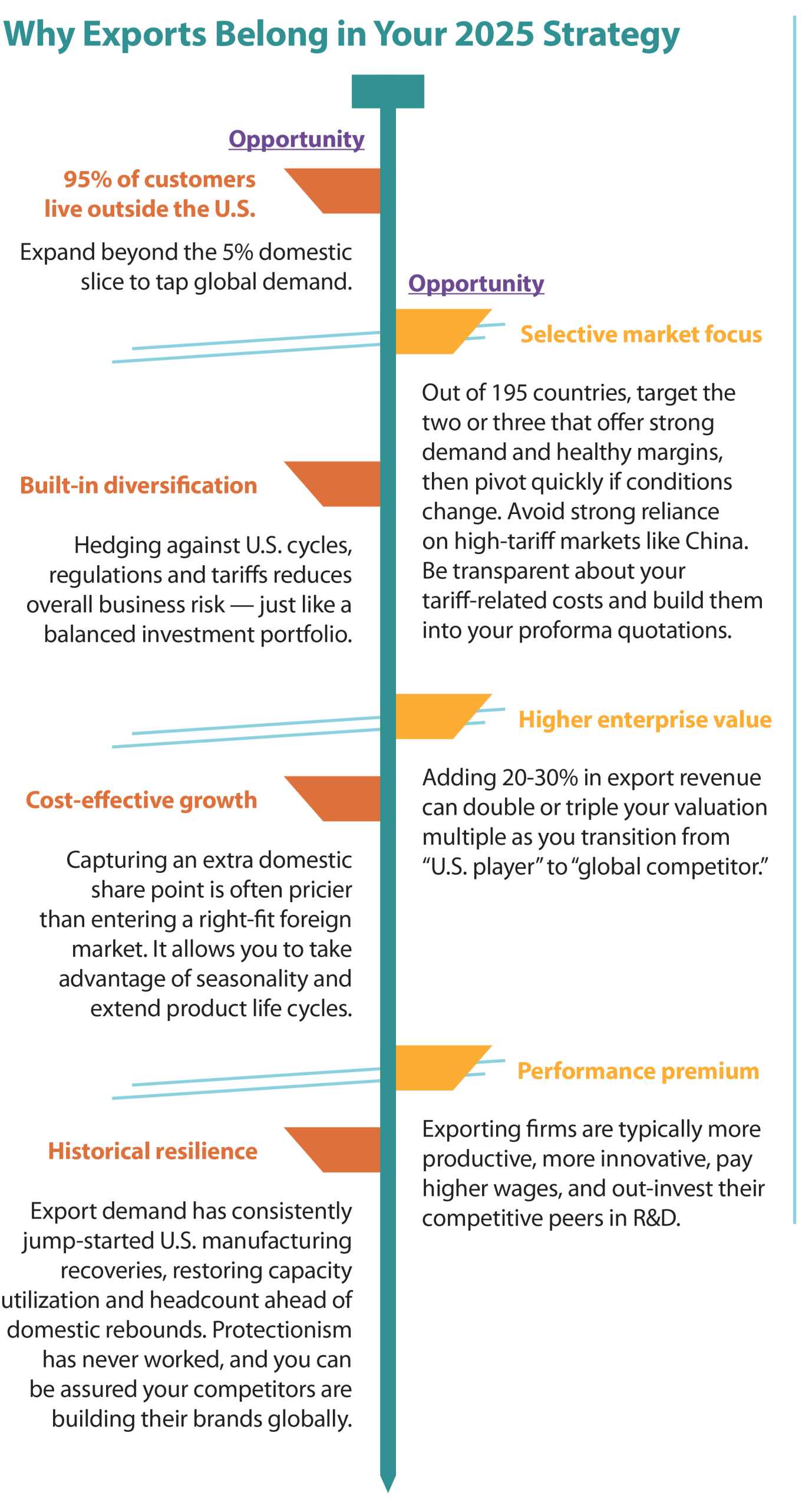

First, from an economist’s perspective, it is important to note that international trade matters greatly to the U.S. and Wisconsin. Trade supports approximately 20% of jobs in Wisconsin. Imports of intermediate goods allow our firms to be cost competitive. Free trade agreements promote access to foreign markets, and foreign-owned companies invest in Wisconsin and employ 136,000 people. Ninety-five percent of the world’s population and 80% of its purchasing power reside outside of the U.S.; future economic growth depends on access to foreign markets.

The trade deficit is generally seen as a macroeconomic phenomenon. If we begin with the equation for Gross Domestic Product (GDP) and do a little rearranging, it can be shown that any trade deficit reflects the fact that we have less private sector saving than investment (which has been the case since the early 1980s) and/or increased federal budget deficits (from the early 1980s through about 1995, and again since 2000). Basically, the rest of the world is lending us money to maintain these deficits.

Over the centuries, economists have refined how they look at trade. We started with the Mercantilist School of thought (attributed to Thomas Mun) in which we “win” by running trade surpluses, and “lose” when we run trade deficits. Though this may sound familiar, it was debunked in 1800. That’s when we looked to the Classical School (Adam Smith), in which we traded based on having a lower absolute cost of producing a good. This was replaced by David Ricardo, who refined Smith’s thinking by considering not absolute costs, but rather lower relative costs (economists consider this in the context of opportunity cost).

When I teach these theories to students, I develop Ricardo’s model looking at trade first between Wisconsin and Minnesota. We see that by specializing and trading based on Ricardo’s theory, folks in both states can consume bundles of goods beyond what they can produce on their own: Trade lowers prices and increases not only how much we can consume, but also the variety of items we can consume. I believe we can all agree these are good outcomes, so when I change the economics from states to nations I ask why there is so much controversy. The economic logic is identical between the two examples. Economists are often criticized for not agreeing on many issues. Having said that, the idea of trade based on comparative advantage being a welfare-enhancing practice is one of the most universally agreed upon economic theories.

Our trade statistics are, as I like to put it, a noisy signal as to the true nature of bilateral trade relations. For example, when we import an iPhone from China, that adds $699 to our deficit. However, China has sourced many components from other nations. Only $8 of value added actually happened in China, so only $8 should be added to our trade deficit.

Another related hot topic is the one of “bringing back jobs.” The U.S. labor market is remarkably fluid. One hundred years ago, roughly 40% of the labor force worked in agriculture. Today, that number is less than 2%. Technological progress has offered far more “creative destruction” to jobs here than trade has. Yet we would never suggest discouraging innovation to preserve jobs. Moreover, in March the U.S. unemployment rate was 4.2%, below the target rate of unemployment. In Wisconsin, it was 3.2%. Based on these statistics, our labor market is strong.

When it comes to tariffs, we are essentially asking ourselves whether we prefer to pay more in taxes. Do consumers like to pay more at the checkout? Do firms like to pay more for the goods they buy in order to produce whatever final good they produce? I doubt either is the case.

Ultimately, economics is about weighing costs and benefits. As I see it, the costs of inhibiting trade are quite high while the benefits of doing so are very low. We tend to think that free trade in markets is a good thing domestically, and I’d argue it extends to the international community as well.

Wisconsin businesses have mixed views on tariffs

by Kurt R. Bauer, President/CEO, Wisconsin Manufacturers & Commerce

The tariff issue reminds me of an old political joke about a congressman who tries to straddle the line on an issue that divides his constituency. “I have friends on this side of the issue, and I have friends on that side of the issue,” he explains. “And I am always with my friends.”

President Trump’s tariffs have put WMC in much the same predicament as that congressman. We have members on both sides of the issue because tariffs affect businesses differently depending on what they make, grow or sell; where they sell it; and where they source components, parts and/or raw materials.

Our members who oppose the tariffs are typically manufacturers who have supply chains overseas and can’t find domestic alternatives for specialty, precision or raw material inputs. One of Trump’s stated objectives in imposing the tariffs is to force those companies to “re-shore” their supply chains, but that is easier said than done. You can’t just snap your fingers and find a new supplier, so you often must pay the tariff. Those higher costs add up, eat into profit margins and create inflationary ripples.

Another concern businesses have with the tariffs is market access. Tariffs provoke retaliation from nations where Wisconsin farmers and manufacturers need to sell their goods. Retaliatory tariffs can make U.S. goods unaffordable. It can also make them undesirable if foreign consumers are angry at the U.S. for imposing tariffs on their nation’s products.

On the flip side, many of our members support tariffs for two major reasons: what they see as fairness, and opportunity for new business.

On fairness, many businesses are fed up with the U.S. opening its markets to foreign-made goods without other nations fully reciprocating. China is the most blatant example. They impose tariffs, manipulate their currency to make Chinese goods less expensive abroad, force technology transfers in exchange for market access or just steal intellectual property through industrial espionage. They also dump products into Western markets below the cost of production to bankrupt competitors, as well as harass foreign businesses operating inside China.

Other complaints include nations imposing value-added taxes (VAT) on U.S. goods, subsidizing specific businesses or sectors and placing various regulatory barriers on imported items.

Trump says other nations don’t play fair, and a sizable number of Wisconsin businesses agree.

Other businesses see opportunity. I have heard from smaller manufacturers, like tool and die and machine shops, that have won contracts because of the tariffs. One told me they received a lucrative contract from a large manufacturer that had been sourcing a part from China. This machine shop will produce the part using the older machines it currently has on its shop floor but, longer term, plans to invest in state-of-the-art machines, as well as the talent to operate them.

As the state’s chamber, WMC’s perspective is that we have been most concerned with three things: supply chain, market access and energy.

I addressed the supply chain already, but a bit more on market access: Wisconsin is a manufacturing and agricultural state. We make things, we grow and process things and we want to sell things around the world. Tariffs threaten access to critical markets, particularly Canada and Mexico — Wisconsin’s top trading partners.

On energy, WMC was initially very concerned when Trump suggested he would impose a 10% import tariff on energy coming from Canada, which is where much of Wisconsin’s fossil fuels are sourced. The president has since backed off, but Wisconsin remains vulnerable.

WMC members have also been frustrated by the uncertainty and confusion the tariffs have created. Still, there has been little panic from the business community. They have been through this before during COVID-19 when supply chains were stressed or broken, and they had to be resourceful and nimble to keep their production lines operating.

One final point: WMC wholeheartedly supports Trump’s objective to grow the manufacturing sector as both an economic and national security imperative. But tariffs alone won’t spark a U.S. manufacturing revival. We need pro-growth policies, starting with reauthorizing the 2017 federal tax reforms, tapping into our vast energy and mineral resources, and reducing the suffocating regulatory burden on business.

Export-led growth: A strategic playbook for CEOs

By Roxanne Baumann, Global Business Strategist, Baumann Global LLC

There’s a mandate for growth. Boards, investors and employees expect sustained, profitable growth — even amid inflation, policy shifts, geopolitical shocks and talent shortages. In a recent manufacturing CEO survey, 68% named growth as their top priority, whether through pricing, new products or acquisition. Yet many overlook one of the most efficient levers: strategic export expansion — executed with best-practice discipline and guided by seasoned expertise. It is much easier to mitigate the risk of tariffs with your export strategy, and it is something you should embrace at this time.

Overcoming the common hurdles

“We lack expertise, bandwidth and a global network. A full‑time hire feels risky.”

- Time-to-revenue reality: Expect a 6-12 month runway to first invoices — but plan for 20-40% faster top-line growth thereafter.

- Fractional expertise: Engage a veteran export executive on a part‑time basis. You gain proven playbooks, in-country contacts and rapid market validation at a fraction of the cost of a full-time headcount. It allows the CEO/CFO to stay focused on the core business while building strategic export markets.

- Best-practice discipline: Skip the “accidental exporter” missteps — no speculative trips, no unfocused distributors and no margin-eroding surprises.

Your next moves

- Quantify the opportunity: Confirm addressable demand, tariff exposure and landed costs for two priority countries.

- Build the business case: Model incremental revenue, margin contribution and valuation impact.

- Secure fractional leadership: Assign a seasoned export director

- to craft and execute a 12- to 18-month market-entry roadmap.

- Learn the playbook: Understand exporting nuances and build your best practices plan that you can repeat as you grow.

- Measure & pivot: Track leading indicators (inquiries, channel readiness, tariff changes, regulatory approvals) and redeploy quickly if conditions shift.

Smart CEOs work smarter, not harder: deploying export expansion as a high-return, low-risk path to sustained growth in 2025 and beyond.

Mid-market manufacturers: 10 steps to reduce tariff exposure

By Jennifer Clement, Client Relationship Leader, CLA (CliftonLarsonAllen)

Since the founding of the United States, tariffs have played a key role in “protecting” industries from more established global competitors. In 1789, George Washington signed into a law a first-ever tariff of 5% on all imports. Since that time, revenue from tariffs has hovered around 2.5 to 5% and has been imposed on everything from nickel to nets to Nintendo.

For the past 250 years, tariffs were used largely for industrial protection. That changed during the first Trump Administration, as they were tailored to advance a policy agenda.

While tariff rules and amounts will likely continue to change, it’s clear tariffs will play a strategic role for Americans at the negotiating table. Those responsible for driving strategy in mid-market manufacturing are understandably finding it hard to read between the headlines and avoid distractions as announcements roll out by geography and by commodity.

Larger manufacturing companies serving global customers have teams focused on mitigating risk and exposure. They have a complex network of options. This is not typically the case for mid-market manufacturers, who may lack the sophisticated resources of larger entities.

In this environment of uncertainty, there are steps mid-market manufacturers can take to mitigate tariffs.

First, on the demand side:

- Map out where your customers are located. What percentage is outside the U.S.?

- Consider if an “in country

- for country” strategy makes economic sense.

- Consider if production for international customers could be configured locally, to free up capacity to keep production for domestic customers in the U.S.

- If speed is key, explore if alliances for serving international customers offer attractive ROI.

Next, on the supply side:

- Determine what percent of your revenue is dependent on goods coming from tariffed countries.

- If you are dependent on one supplier, consider immediate action to find alternate sources elsewhere, including domestic.

- Break down imports by raw material, components, sub‑assemblies and finished goods.

- Be ready to manage different tariff levels for each, and renegotiate contracts if changes in pricing, terms and deliveries make sense.

- Break out costs by material goods and services. Services are typically not tariffed. A trade attorney can sort through details.

- Map out global workflow. If a sub‑assembly has a stop in Mexico on its way from China to your U.S. dock, confirm it meets the U.S. definition of “significant transformation” before crossing our southern border and being subject to an additional tariff. Relatedly, evaluate the number of times each build crosses a border. Some complex assemblies, for example, can cross a border five to six times prior to completion of a finished good. Can steps be eliminated? Finally, consider if Free Trade Zones — where items can be processed/stored, etc. — offer potential benefits. Again, trade attorneys can be helpful with details.

- Scrutinize inventory management. When was the last time you did an ABC analysis? In this environment where costs can change overnight, getting back to basics is critical. For A items, it may make sense to stock up before tariffs hit, or quickly burn off stock of C items.

- Consider where and how it makes economic sense to move production as close to the customer as possible.

For those who depend on imports, tariffs will lead to higher costs, margin erosion and pressure to address pricing. Conversely, tariffs may open opportunities for those with capacity to develop into local sources for their own companies and others.

Diversifying supply chains takes time. Many manufacturers who started the process back in 2016 as the first wave of policy-driven tariffs surfaced are having to completely rethink supply chains now. It’s a moving target.

Don’t let your organization and customers feel the weight of tariffs — enact risk mitigation strategies to strengthen your business and manage rising costs.

The tariffs that were supposed to help us

by Sachin Shivaram, CEO, Wisconsin Aluminum Foundry

We are the kind of company that should be thriving under President Trump’s tariffs.

At Wisconsin Aluminum Foundry, we melt aluminum and cast it into precision parts for trucks, medical equipment and satellites at our facilities across the northern Midwest. Our inputs are sourced locally. Our labor is old-fashioned American industrial grit. Our customers are national champions of industry. We are the poster child for the type of company the president seeks to support.

In theory, the steel and aluminum tariffs imposed under Section 232 of the Trade Expansion Act should boost our production.

Reality has turned out to be different.

When Trump won the election, like many manufacturers, we were hopeful. The prior two years had brought shrinking demand for manufactured goods. The morning after the election, I sent a gushing note to employees saying that while I had voted differently, I was excited for what might come. Tariffs could spur reshoring. Tax cuts and deregulation might lift business sentiment. As we waited for clarity on the president’s policies, I wrote in a LinkedIn post that it felt like metal manufacturing in America was on the cusp of renewed vitality.

Six months into his presidency, that optimism has faded. U.S. manufacturing has stalled, input costs from tariffs are rising at the fastest rate in nearly two years, business investment has slowed and demand readings hover at contraction levels.

What became clear when the president finally announced his tariff policy is that it lacks any genuine understanding of the businesses it claims to support.

A few weeks ago, I joined 15 other industrial CEOs for a meeting in Washington, D.C. We hosted one of the top congressional Republicans. She began by saying she meets with the president two or three times a week and that he remains firmly committed to the tariffs he launched on “Liberation Day.” It was meant to be reassuring.

It wasn’t. Her comments landed with a thud. The room, filled with manufacturing executives from across the country — including the CEO of one of the largest Wisconsin manufacturers, many of them longtime conservatives — went silent. After she left, one CEO turned to me and said, “Wow, that was frosty.”

The sentiment wasn’t anger; it was disorientation.

What should have been a home-field crowd felt anything but. These are the people the policy is supposed to help. And yet none of us supported the tariffs. Not even a company like ours, which arguably benefits the most. Even the venerable National Association of Manufacturers opposes the tariffs. It may surprise you to learn that our voices aren’t part of the conversation.

The tariff policies are increasingly looking like the misguided conviction of one person: the president. Even among his political allies, there is no real support. Congress has taken no action to codify this approach into law. Instead, the future of the tariffs is being fought over in courtrooms. Seemingly, there is no serious constituency behind this policy other than President Trump himself.

The deeper irony is this: We’ve always said uncertainty is bad for business. But at this point, the bigger fear is that the uncertainty might end, and we’ll be left with certainty around bad policy.

We saw it again May 31, when Trump doubled the Section 232 aluminum tariffs from 25% to 50%. The stated goal was to revive domestic smelting. But since he first launched aluminum tariffs in 2018, one U.S. smelter has shut down and two more have gone idle. Not a single new smelter has broken ground. Why would they? Building one costs $4 to $6 billion and takes five years. And in an energy-intensive industry like ours, no company is going to make that bet without a long-term national strategy to produce lower-cost electricity.

Meanwhile, aluminum costs have spiked. The Midwest premium has nearly tripled this year, putting pressure on every industry that relies on aluminum, from automakers to aerospace suppliers. Customers are putting programs on hold. Costs are up. Demand is falling. We recently announced layoffs at our plants in Indiana and Iowa, the first time we’ve reduced headcount after a year of steady growth.

This is what a flawed policy looks like on the ground.

One of our customers in Florida builds power equipment for AI data centers. He approached us to reshore a casting program currently being produced in Canada. In theory, the tariffs should have made our offer more attractive. But when we submitted our quote, we couldn’t come close. The very tariffs meant to help us had raised input costs to the point that we were no longer competitive.

This is the complexity the current policy refuses to acknowledge. Manufacturing supply chains are deeply interconnected. You can’t bludgeon one link in the chain and expect the rest to fall into place.

Tariffs can be useful. But they are not a substitute strategy. What we need is a clear national industrial policy, one that identifies sectors vital to our economic and national security, and then supports them with targeted tools: public investment, tax credits, workforce development, R&D — and yes: tariffs, too.

At Wisconsin Aluminum Foundry, we’ve expanded our capacity, acquired new capabilities and hired hundreds of workers in the past few years. We’re ready to keep investing. We need policymakers to match our seriousness. That means articulating long-term goals and creating the conditions for domestic industry to compete fairly, strategically and sustainably.

If even a company like ours, the supposed winner from tariffs, is struggling to find a benefit, it’s time to ask: Who, exactly, is this policy helping?